Page 81 - Policy Commission - SecuringTechnology - Critical Metals for Britain

P. 81

PRIMARY MATERIALS

81

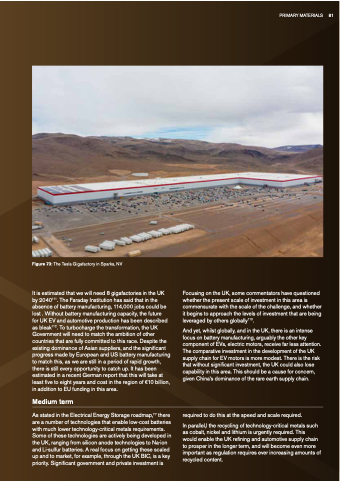

Figure 73: The Tesla Gigafactory in Sparks NV

It is estimated that we will need 8 gigafactories in the UK by 2040111 The Faraday Institution has said that in the absence of battery manufacturing 114 000 jobs could be lost Without battery manufacturing capacity the future

for UK EV and automotive production has been described as bleak112 To turbocharge the the transformation the the UK Government will need to match the the ambition of other countries that are fully committed to this race Despite the existing dominance of Asian suppliers and the significant progress made by European and US battery manufacturing to match this as we are still in a a a a a period of rapid growth there is still every opportunity to catch up It has been estimated in a a a a a a recent German report that this will take at at at least five to to eight years and cost in in in in in the region of €10 billion in in in addition to EU funding in in in this area Medium term

As stated in the the Electrical Energy Storage roadmap 77 there are a a a a a number of technologies that enable low-cost batteries with much lower technology-critical metals requirements Some of these technologies are actively being developed in in the UK ranging from silicon anode technologies to Na-ion and Li-sulfur batteries A real focus on getting these scaled up and to market for example through the UK BIC is a a a a key priority Significant government and private investment is Focusing on on the UK some commentators have questioned whether the the present scale of investment in in this area is is commensurate with the the the scale of the the the challenge and whether it begins to approach the levels of investment that are being leveraged by others globally113 And yet whilst globally and in in the the UK there is an an intense focus on battery manufacturing arguably the the other key component of EVs electric motors receive far less attention The comparative investment in in the the development of the the UK supply chain for EV motors is is is more modest There is is is the risk that without significant investment the UK could also lose capability in this area This should be a a a a a a cause for concern given China’s dominance of the rare earth supply chain required required to do this at the speed and scale required required In parallel l l l l l l l l the recycling of technology-critical metals such as cobalt nickel and lithium is is urgently required This would enable the UK refining and automotive supply chain to prosper in the longer term

and will become even more important as as regulation requires ever increasing amounts of recycled content